1. Introduction

“Financial technology” or “Fintech,” the field of utilizing technology to provide financial solutions, grew hugely in popularity in 2014. Within one year, from 2014 to 2015, Fintech startups increased significantly, and traditional financial institutions opened new Fintech services, with investments ranging from $12 to USD 197 billion

| [27] | Arner, Douglas W., Janos Barberis, and Ross P. Buckley. "The evolution of Fintech: A new post-crisis paradigm." Geo. J. Int'l L. 47 (2015): 1271. |

[27]

. In such a period of growth and innovation, quantitative finance garnered attention from industry players and consumers.

In this paper, quantitative finance refers to both quantitative trading–trades of data–and cryptocurrency–trades of digital currencies.

Quantitative finance emerged from the work of Louis Bachelier–an early 20th-century mathematician–on option pricing, which economists like Paul Samuelson and Robert Merton later rediscovered. Contributions from Harry Markowitz’s portfolio optimization and Edward Thorp’s adaptation of blackjack strategies led to its evolution, culminating in the Nobel-winning Black-Scholes model, pivotal in modern quantitative strategy, including those in cryptocurrency

. 2015 saw increasing interest in quantitative trading precisely because of the following three reasons:

1. Market volatility: The Chinese Stock Market Crash in August increased unemployment in the traditional finance industry, prompting the development of new Fintech startups. Since models were needed to predict market performance and prevent financial instability, many people transitioned from exchanges or banks to establish their quantitative trading firms.

2. Policy changes: Many global central banks, including the European Central Bank and the Bank of Japan, implemented quantitative easing policies to lower borrowing costs and stimulate the economy.

3. Technological advancement: 2015 marked the development of machine learning and artificial intelligence techniques

, with new products–such as TensorFlow and Kera crucial for backing quantitative trading–entering the market.

Section 1 will briefly describe quantitative trading, its business model, and its advantages over traditional banking practices and other digital technologies. In section 2, this paper will discuss the implications of quantitative trading and its regulatory challenges compared to other digital technologies. Section 3 will compare cryptocurrency with quantitative trading, with a clear distinction that quantitative trading firms are data-driven brokerage firms and cryptocurrencies are financial instruments, and discuss the negatives of cryptocurrency. In the conclusion section, this paper will first synthesize the pros and cons of each subject and then give a prognosis of the Fintech industry.

2. Introduction to Quantitative Trading and Its Advantages

2.1. A Brief Description of Quantitative Trading

Quantitative trading refers to digital trading between stockbrokers and individual or institutional clients in the financial markets guided by mathematical and statistical models

| [67] | Stoikov S, Waeber R. Reducing transaction costs with low-latency trading algorithms [J]. Quantitative Finance, 2016, 16(9): 1445-1451. |

[67]

. As suggested by its name, quantitative trading is centered around data. Unlike conventional trading methods, which heavily depend on human judgment and market analysis, quantitative trading harnesses algorithms to analyze extensive data sets, striving for rapid and efficient transactions. Quantitative traders first collect data from financial markets that indicate historical prices, trade volumes, and market trends, then develop mathematical models to analyze these data sets, test their models' effectiveness using past data, and then automatically execute trades according to the signals produced by the model.

Technological Advancements

Quantitative trading heavily relies on sophisticated software tools, programming languages, and AI technologies

. Below is one example of each:

(1) Metatrader: a trading platform (software tool) that provides access to stocks and produces algorithms for Forex traders, who exchange fiat money online

.

(2) Python: a programming language that helps quantitative traders write scripts, fetch and analyze data, and guides users when using the platform

| [77] | Zhang P, Gao Y, Shi X. QuantCloud: A software with automated parallel python for Quantitative Finance applications [C]//2018 IEEE International Conference on Software Quality, Reliability and Security (QRS). IEEE, 2018: 388-396. |

[77]

.

(3) TensorFlow: a platform that focuses on deep learning and neural networks and develops AI models to predict and memorize market trends.

The advantages of these technologies applied to quantitative trading will be explained in the following subsection.

Quantitative trading firms develop trading systems and algorithmic platforms for brokerages and clients. They gain revenue in two main ways

:

1. Commissions: Quantitative traders usually charge a fee based on the volume or value of the stocks or securities traded through the algorithmic platform owned by their firm.

2. Shares: In addition to their relations with brokerage firms, many quantitative traders gain shares by matching buy and sell orders on the exchanges' platforms.

In addition, some quantitative trading firms have launched a new business model for selling financial market data. For instance, Shanghai Quant360 Information Technology Company provides data content services and digital platform tools. From the extensive databases his company is connected to, his company facilitates a range of financial instruments like "stocks, mutual funds, bonds, options, futures, and more." Additionally, it accommodates diverse data types, including "market quotes, fundamentals, and others

.”

2.2. Advantages of Quantitative Trading Over Traditional Trading Practices

2.2.1. Algo-Based Trading

Traditional trading involves a hands-on approach, with human traders analyzing market data, economic indicators, and various factors to decide when to buy or sell assets

. Again, traditional trading methods are often more subjective, making trades susceptible to human judgment. For instance, people may buy what they have purchased earlier and was economical for them or what they believe is in flow with market trends and price movements. Even though relying on market trends and price movements makes decision-making more flexible, this manual approach can result in a huge issue–human error

.

Quantitative trading minimizes human error because AI helps quantitative traders make decisions or even makes decisions for them through the algorithmic models it has developed. AI does not experience fatigue and is less likely to make errors such as mistyping trade volumes

.

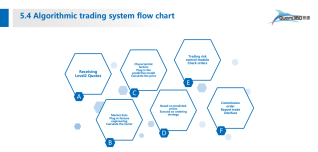

Figure 1 below shows how the SFATS algorithmic trading system of Shanghai Quant360 Information Technology Company functions internally:

Figure 1. 6 Steps to Execute Trades of Shanghai Quant360 Information Technology Company. (Source: Quant360 Products Information).

As shown by

Figure 1, SFATS does all the preparation work before placing the orders onto the rapid trading system

.

In addition to offering more accurate data before, during, and after trades, AI-based quantitative trading predicts the fluctuating values of stocks in the market

| [74] | Wangpaichitr K. How effective is' relationship marketing'in gaining customer loyalty to securities brokerages? [D]. Northumbria University, 2010. |

[74]

. One of the leading causes of the 2015 Chinese Stock Market Crash was that global investors sold the oil stocks that were unexpectedly declining in value

. Quantitative trading minimizes the impact of the price uncertainty of stocks through the Long-Short Term Memory (LSTM) model, a Recurrent Neural Network (RNN) that memorizes data and identifies market trends. The LSTM model filters data to prioritize the processing of volatile stocks

, making intelligent modeling, including a multidimensional check, more efficient

| [64] | Information Technology Co..Ltd Products Introduction V2.7-20240531.pdf. |

[64]

.

Some quantitative trading firms have upgraded the LTSM model to the Attention-LTSM model to account for human sentiments. Human traders are more likely to pay attention to the prices of securities that are market indicators or particular exchanges. For instance, an individual Chinese stock investor will focus on the prices of stock of Huawei, a cornerstone company for the Chinese economy, and Huawei will focus on its performance with Western competitors in the US market

| [52] | Liu X. Chinese multinational enterprises operating in western economies: Huawei in the US and the UK [M]//China’s Big Power Ambition under Xi Jinping. Routledge, 2021: 219-236. |

[52]

. This Attention-LTSM model assigns weights of importance to data information based on the results parsed by AI, helping human traders select stocks more quickly and enhancing the client’s portfolio

| [73] | Waisi M. Advantages and disadvantages of aI-based trading and investing versus traditional methods [J]. 2020. |

[73]

.

Whether traditional floor trading or innovative online trading, most human traders do not trade much to avoid risks because they lack knowledge of the market dynamics, or some trade too much because of their biases, greed, or overconfidence

| [50] | Leaver M, Reader T W. Human factors in financial trading: An analysis of trading incidents [J]. Human Factors, 2016, 58(6): 814-832. |

[50]

. An underutilization of trading and an overutilization of trading can lead to slower growth of wealth and dependency issues respectively

| [71] | Thompson K W, Shea T H, Sikora D M, et al. Rethinking underemployment and overqualification in organizations: The not so ugly truth [J]. Business Horizons, 2013, 56(1): 113-121. |

[71]

. Dependency in traditional trading refers to one trader overly relying on another trader’s goods; this leaves one trader vulnerable to price fluctuations and disruptions in supply chains

| [30] | Birdsall N, Hamoudi A. Commodity dependence, trade, and growth: when'openness' is not enough [J]. Center for Global Development Working Paper, 2002 (7). |

[30]

. This can be costly for one trader when suffering from the depreciation of goods and monopolies. Not to mention that since free-floating exchange rates are present, these risks are aggrandized in traditional international trade. In summary, the pivot of these issues is a lack of precision that decreases the trust of human traders in themselves.

Algo-based quantitative trading offers this precision through mathematical models and an enhanced combination of financial assets processed by AI and other information technologies

| [68] | Ta V D, Liu C M, Tadesse D A. Portfolio optimization-based stock prediction using long-short term memory network in quantitative trading [J]. Applied Sciences, 2020, 10(2): 437. |

[68]

. A human trader can only predict the profit-maximizing quantity of trades with the help of a well-researched, objective, and adaptable mathematical formula. This increases human traders’ confidence in themselves, helping to facilitate the sustainable growth in their wealth; meanwhile, as human traders use more of the algorithmic trading systems owned by quantitative trading firms, they pay more commission fees–a win-win situation is realized, with human traders gaining more economic revenue and quantitative trading firms gaining more commercial revenue. As for the three parties involved in trading, quantitative trading optimizes the number of transactions and the volumes within one trade

| [31] | Brownlees CT, Cipollini F, Gallo G M. Intra-daily volume modeling and prediction for algorithmic trading [J]. Journal of Financial Econometrics, 2011, 9(3): 489-518. |

[31]

.

AI-backed quantitative trading can consider more financial factors than traditional trading methods. Quantitative traders devise an execution strategy tailored to market microstructure, the branch of finance that analyzes the impact of trading mechanisms on the prices of stocks, securities, or bonds

. This execution strategy, backed by computations, helps human traders know when to use market orders, which refer to buying or selling securities at their best market price, or limit orders, which refer to buying or selling securities at specific prices

. Limit Order Book (LOB), a collection of limit orders, tells quantitative traders a stock is illiquid if its volume at each quote is low or the bid is low and the ask is high

. Because AI can use historical data to predict the liquidity of stocks based on their trading volumes and bid-ask spreads, quantitative trading delves into another variable that is only determinable with data, perfecting the portfolio.

The trading transaction costs positively correlate with market volatility and price discrepancy

| [54] | Marshall B R, Nguyen N H, Visaltanachoti N. Commodity liquidity measurement and transaction costs [J]. The Review of Financial Studies, 2012, 25(2): 599-638. |

[54]

. Quantitative trading minimizes transaction costs because AI can use historical data to predict market volatility. Al-powered Transaction Cost Analysis (TCA) evaluates the performances of the algorithmic trading strategies in use and refines them respectively based on price impact, fill rates, and execution speed

| [42] | Duran A, Bommarito M J. A profitable trading and risk management strategy despite transaction costs [J]. Quantitative Finance, 2011, 11(6): 829-848. |

[42]

; moreover, TCA analyzes the performances of exchanges by putting stocks into the “trade” or “no trade” region and aiming to minimize the risks posed by volatility and liquidity

| [67] | Stoikov S, Waeber R. Reducing transaction costs with low-latency trading algorithms [J]. Quantitative Finance, 2016, 16(9): 1445-1451. |

[67]

. Shanghai Quant360 Information Technology Company employs TCA to improve its algorithmic trading strategies and select high-performing stockbrokers. Backed by fast programming languages, including Python and Java, Shanghai Quant360 company resolves the latency issue that delays transactions and disperses the LOB, making the market less transparent for traders and decreasing both physical and opportunity costs. The advantages of the company’s employment of TCA will be explained more thoroughly in the following subsection, with a focus on the benefits of the company's closer relations with financial institutions, particularly stockbrokers.

Consider the reflections that students do after a math class: reflections help students avoid some repeated mistakes, but not all are promised. One can only remember the trigonometry part, which challenges them the most, and one can only remember the algebra part. This is akin to trading in the open market. Since the human brain cannot memorize the information of every stock, and new stocks constantly enter the market, humans need backtesting, a retrospective model that rates the performances of current algorithmic strategies using past data and produces the results of profit, success rate, and downturn

. In Monte Carlo simulation, for instance, market data samples are randomly created using statistical distributions and parameters from past data

. This type of backtesting renders quantitative trading another asset because traders can spot outliers and unusual incidents and adapt to disparate market conditions. Backtesting works if there is data, and it even tells human traders that they should start with the data two or three months ago if deciding to employ a day trading strategy

. However, excessive backtests can be harmful as they increase the likelihood of overfitting

, and I delve into this phenomenon in section 2.

In brief, the synergy between algorithms and models, driven by programming languages and AI, enables quantitative trading to predict volatility, liquidity, and uncertainty based on trade prices, quantities, and volumes. This optimizes portfolios, boosting investor confidence and driving profits for all parties involved in quantitative trading.

2.2.2. Rapid Trading System

Quantitative trading companies function as venues, and their products are considered infrastructures

. Besides the algorithms and models they offer, their core product is a rapid trading system

.

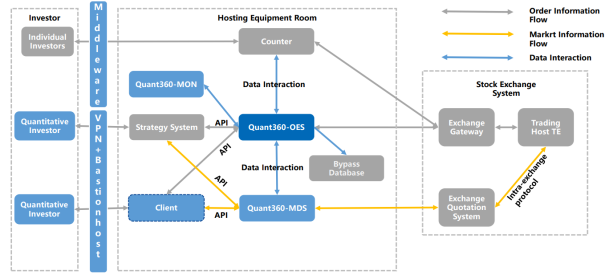

Figure 2 below shows how the Ultra-Speed Trading System of Shanghai Quant360 Information Technology Company functions internally:

Figure 2. The Internal Structure of The Order Execution System (OES). (Source: Quant360 Products Information).

The core product of the Ultra-Speed Trading System, as shown, is Quant360-OES, or the Ultra-Speed Order Execution System. The core services of OES include “order reception, real-time risk control, order declaration, collection of declaration confirmation, transaction return collection, and execution report push,” and some of its auxiliary services and management services include trading inquiry and system monitoring, respectively

. The following data perfectly interprets that quantitative trading is rapid and frequent

| [64] | Information Technology Co..Ltd Products Introduction V2.7-20240531.pdf. |

[64]

:

1. The internal processing of OES reduces delays of older versions by 60.9 percent.

2. The latency for OES bond trading is 1.5 milliseconds, compared to the traditional online trading average latency of 30.0 milliseconds.

3. 1.5 million orders are executed per second in OES.

4. “The uplink delay for the Shenzhen Stock Exchange trading gateway” has been fine-tuned to 15-16 microseconds.

This trading efficiency gained the company international attention: in 2020, when the financial market presented a decline, the company became one of the two data providers for a stockbroker giant in the United States

. The CEO says that this achievement can be attributed not only to their OES but also to their API.

As shown in

Figure 2, API, standing for Application Programming Interface, consists of guidelines and protocols facilitating the interaction between software applications, allowing them to exchange data, functionalities, and features

. Since Shanghai Quant360 Information Technology Company is not publicly traded, API allows the overclocking machine, Python, and Tensorflow to communicate with each other, making the quantitative traders more responsive to payment information. API functions as a means to advertise the company’s products, collaborate with external stakeholders, expand offerings, and reach new markets. Moreover, since API activation needs authentication, it simultaneously protects the company’s private information.

As of 2024, Shanghai Quant360 Information Technology Company has worked with 20+ Chinese securities brokerage firms

. Having close relationships with these stockbrokers gives the company two other advantages: the first benefit is cultivating stronger connections with a broader customer base, achieved through Relationship Marketing (RM)

| [74] | Wangpaichitr K. How effective is' relationship marketing'in gaining customer loyalty to securities brokerages? [D]. Northumbria University, 2010. |

[74]

, which links customers to the company via reputable stockbrokers. This leads to elevated trading volumes and profits. Securing access to broader investments is the second benefit. As stockbrokers increasingly trust quantitative trading companies, private investors seeking greater returns and investment banks interested in Initial Public Offerings (IPOs) become more inclined to provide direct funding and IPO opportunities, respectively.

3. Disadvantages and Risks of Quantitative Trading

As mentioned in the previous subsection, excessive backtests increase the chance of overfitting, the concept that the algorithms become overly tailored to its training data, causing the model to struggle in making accurate predictions or drawing conclusions from Out-Of-Sample (OOS) datasets

| [48] | IBM. “What Is Overfitting? IBM.” www.ibm.com/topics/overfitting |

[48]

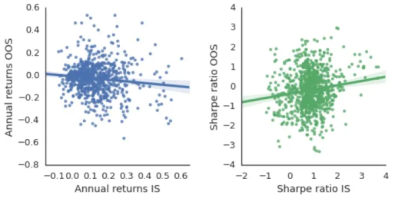

, which can result in financial risks. Quantitative traders trust the sample datasets because they believe the models can function generally due to their historical sound performances. Risk analysts often employ the Sharpe Ratio to quantify the additional return an investment generates per unit of total risk it incurs

.

Figure 3 compares algorithm performances based on in-sample (IS) and out-of-sample (OOS) datasets using annual returns and Sharpe Ratio.

Figure 3. OOS’s comparison with IS by two metrics: annual returns and Sharpe Ratio (Source: curtisnybo.com).

The analysis of each graph is presented as follows:

The slight negative correlation between Annual Returns OOS and Annual Returns IS suggests that algorithms performing strongly in backtests using IS datasets cannot guarantee sound performances in real-world scenarios where datasets become random

.

The slight positive correlation between Sharpe Ratio OOS and Sharpe Ratio IS is due to the difference between annual returns and risk-free rate increasing faster than the likelihood of volatility, causing both Sharpe ratios to increase. However, since the difference between Sharpe Ratio IS and Sharpe Ratio OOS is rising, this suggests an unexpected occurrence of volatility in real-world scenarios that algorithm developers who maximize returns fail to consider. The Sharpe ratios graph also indicates that less money is gained from OOS datasets than IS datasets since the IS Sharpe ratio deviates from the average return more positively than the OOS Sharpe Ratio.

The increase in the numeral difference between Sharpe Ratio IS and Sharpe Ratio OOS suggests that as the timeframe of backtests and the reliance on IS datasets increase, the likelihood of overfitting and its impact increase, causing more failures of backtesting algorithms that may lead to lower annual returns, lower risk-free investment returns, and higher volatility. Besides, the point protectors are dispersed throughout each graph and show a less than 0.25 relationship with the line of the best fits

, suggesting that less than 25 percent of the dependent variable OOS performances can be explained by the analyzed metric, which further corroborates the argument against the potential for predicting OOS profitability using backtest data. Nassim Taleb, an American mathematical statistician and risk analyst, says, “If you want to bankrupt a fool, give him lots of information

.”

Contrary to the quote above, a lack of information can also lead to bankruptcy. Overfitting fixates on single algorithms and datasets, leading to inaccurate prices, quantities, and volume predictions. This undermines portfolio performance by reducing liquidity and increasing volatility. However, regular backtesting every six months

, assessing the performance of various algorithms using both in-sample (IS) and out-of-sample (OOS) datasets, can prevent overfitting.

Quantitative trading is subject to blackswans--which are sudden and unforeseen events including an unexpected occurrence of volatility in the market--that can incur significant financial losses

. Few experiments or research have been done to guarantee the stability of new software systems. When these software systems are applied, quantitative traders have the knowledge but not the experience. Because of this, quantitative trading is subjected to computer glitches or a failure of the computer system

. Since humans are still responsible for the coding, a small error in coding–such as misplacing the parenthesis–can lead to a colossal miscalculation, contributing to blackswan events. A malfunction in computerized trading operations at Knight Capital, a U.S. financial services firm, caused the 2012 stock market disruption and resulted in approximately 440 million dollars in losses for the company

.

Quantitative trading is capital-intensive because building the software systems requires significant money

. Because of this, a quantitative trading start-up needs intensive capital layouts from banks and partners.

Long-Term Capital Management (LTCM) was a prominent U.S. hedge fund that used mathematical models to make highly leveraged bond bets and other financial instruments

. LTCM did not prepare well for the 1998 financial markets crisis because, while LTCM was repaying debt to its investors, it was using the borrowed money to expand the scale of its investments

. This increased the already high leverage, which resulted in high losses when the returns from investments became lower than the loan interest

. Furthermore, the spreads diverged instead of converging

. As the financial markets crisis intensified in August 1998 due to the depreciation of the Ruble

, LTCM immediately lost 553 million dollars, about 15 percent of its assets

.

Therefore, the lesson learned is that quantitative traders must pay attention to corporate leverage and, again, the number of backtests to avoid failed investments. However, mathematical models enhance decision-making since quantitative trading platforms are data-driven infrastructures. Cryptocurrency, by comparison, depends more on subjective speculative decision-making. European Central Bank President Christine Lagarde, U.S. Treasury Secretary Janet Yellen, and U.S. Senator Elizabeth Warren all characterized Bitcoin, the first and the highest value cryptocurrency in the world

, as a “highly speculative asset

| [33] | Casey, Michael J. 2021. “Money Reimagined: Crypto Speculation Is a Feature, Not a Bug.” March 5, 2021. |

[33]

.” This, in turn, makes it more susceptible to financial crises and losses.

Quantitative trading requires intensive physical capital and human capital. Since quantitative traders are responsible for setting the demands and managing the software systems

| [76] | Xiao X. High frequency trading system design and process management [D]. Massachusetts Institute of Technology, 2009. |

[76]

, they should be good at basic math and science and understand programming languages and code. 95 percent of Shanghai Quant360’s employees know how to code, and 90 percent of them majored in computer science

. The remaining 10 percent of those who know how to code but did not major in computer science taught themselves programming.

The high demands of quantitative trading companies require facilitators to have many data-based and analytic skills, as opposed to traditional trading, which allows anyone who knows the market, has assets for trading, and is interested in making money to be a trader. Quantitative traders make little money from trading because the commissions are for the company, not individual traders, unless they invest in financial instruments. Moreover, employees must be proficient in coding and modeling and should understand the terminology of proprietary financial instruments. Regulators should be more strict in recent years since COVID-19 has increased the number of disqualified quantitative traders and cases of illegal quantitative trading practices.

Since quantitative trading centers around data, it faces the risk of unauthorized disclosure of information. As mentioned earlier, authentication prevents information leakage caused by hacking and involuntary leakage. Still, it cannot prevent a data breach if a quantitative trader inside a transaction voluntarily leaks the information to investors outside the transaction. This occurs because of the mutualistic relationship between the insider and the outsider. Consider this scenario: an outside investment banker releases signals to inform an executive of a quantitative trading company market changes, which helps the executive avoid risky assets and make better investment decisions; in return, the executive who is the only one in the company who has access to Material Non-Public Information (MNPI)

, or private information of a company that can influence its stock price and decisions on investments, leaks MNPI to that investment banker before it becomes known to partners, and this unfair advantage incentivizes the outside investment banker to make private equity investments

| [51] | Liu X, Huang W, Liu B, et al. Strategic leakage of private information [J]. The North American Journal of Economics and Finance, 2019, 47: 637-644. |

[51]

.

Quantitative trading should not be regulated like traditional banking. Regulators should refrain from entirely using the Basel Framework to oversee quantitative trading activities because Fintech is not mentioned in the framework, and quantitative trading is data-driven instead of money-driven by nature. Furthermore, the Basel Framework is outdated and does not consider many external factors.

Quantitative trading companies should still comply with the supervisory standards of federal agencies like the Securities and Exchange Commission (SEC) because they are still tied to investors' interests. And since quantitative trading, like many other financial technologies, is borderless, quantitative trading companies should adhere to countries’ local laws and be overseen by their regulatory bodies

| [21] | “What Are the Regulatory Considerations for Quantitative Trading?” n.d. Quantitative Trading. Accessed June 17, 2024. |

[21]

. Because they are aligned with clients' financial goals, quantitative trading companies should regularly conduct audits and thorough reporting while offering education on the strengths and weaknesses of their algorithms and models

. This is essential to uphold clients’ confidence and protect them from unfair trading practices caused by humans, including insider trading. Shanghai Quant360 Information Technology Company has testing and maintenance departments

, and these two components underscore the importance of regularly inspecting and repairing the company's products.

Regulators should pay attention to the creation of comparative advantages within the trading industry caused by advanced technologies. Because of its use of advanced technologies, quantitative trading rapidly absorbs data, which allows it to leverage latency arbitrage, a trading strategy that exploits delays in executing trades

, to gain profits from the decrease in stock price within microseconds. Advanced technologies give quantitative trading rapidness, frequency, vast and precise data, and the ability to predict the market; however, quantitative trading should not utilize the technologies to travel in time and escape from reality. Therefore, regulators should consider enacting a law that bans leverage arbitrage.

4. Cryptocurrency vs. Quantitative Trading: Comparisons

4.1. A Brief Description of Cryptocurrency

A cryptocurrency is a virtual currency that functions on decentralized networks backed by blockchain technology, wherein collections of financial accounts are spread across various computers

. Cryptocurrencies are created by declassifying mathematical puzzles using codes, models, and algorithms, and creators–or miners–are incentivized to do so to acquire Bitcoin from exchanges

. Intended users use fiat money to buy cryptocurrency from exchanges and brokers, and they then store them in "hot" or "cold'' digital wallets–the former has a connection to the internet, and the latter does not have a connection to the internet

. Hacking is possible but not likely to occur even in hot wallets because, as part of its name, “crypto,” suggests, encryption algorithms protect the transaction histories of cryptocurrency trading by giving the deciphering key to only the intended buyer, which makes information anonymous and secure

| [74] | Wangpaichitr K. How effective is' relationship marketing'in gaining customer loyalty to securities brokerages? [D]. Northumbria University, 2010. |

[74]

.

Differences From Quantitative Trading

Before delving into what differentiates cryptocurrency from quantitative trading, both cryptocurrency and quantitative trading fall into the category of quantitative finance, an innovative branch of finance that employs algorithms, models, and codes to learn and utilize the financial markets

. Moreover, both cryptocurrency trading and quantitative trading are supported by two information technologies: cloud computing and API. Cloud computing assists crypto mining and enables the verification of cryptocurrency accounts, and cloud computing services from corporate giants like Microsoft, Google, and Amazon facilitate massive and intricate computations without mature infrastructure for quantitative trading companies

.

Like stocks, securities, and bonds, cryptocurrency is a financial instrument–monetary assets available for buying and selling

. Accordingly, the purpose of buying or selling a cryptocurrency, similar to buying or selling a stock, is to make profits

. Holders of cryptocurrencies invest them in businesses and wait for high returns. Cryptocurrencies are free of government control, which, by extension, suggests that a decrease in tax or an increase in investment spending will not automatically stabilize their prices, further making cryptocurrencies volatile

. Moreover, unlike quantitative trading, cryptocurrency trading is highly speculative; in other words, buyers or sellers rely solely on the price fluctuations of cryptocurrencies rather than their fundamental values, including returns on investments

. The laws of supply and demand determine the prices of cryptocurrencies. If holders of Bitcoin, for instance, sell due to foresight for financial crises, the remaining holders raise the cost thereof. If the value of a particular cryptocurrency increases, confident investors will buy more of that than its substitutes. However, precisely because cryptocurrency trading is highly speculative, this exacerbates the already volatility. I will delve into the implications later.

Investors buy cryptocurrencies to profit because they believe cryptocurrencies can safeguard their investments' returns from inflation. Unlike fiat currencies, which can be printed by central banks as much as they wish, the number of cryptocurrency coins is either fixed or maintained

. For instance, Bitcoin is capped at 21 million coins

. However, although the U.S. Treasury may agree that cryptocurrencies are hedges against inflation, no empirical evidence has corroborated the argument since cryptocurrencies were born in the decade in which inflation is inconspicuous.

Cryptocurrency is a financial instrument that can be traded, leading quantitative trading companies to build data-driven, AI-powered infrastructures, which will facilitate trades of financial instruments like cryptocurrencies and other assets. Blockchain networks connect nodes or computers that discharge the same orders, making cryptocurrency trading a peer-to-peer (P2P) practice. Herein, it means that cryptocurrency sellers are directed to intended buyers in the absence of intermediaries, and by extension, transaction costs. On the contrary, platforms built by quantitative trading companies are intermediaries who charge commission fees but do not often profit from the trades themselves.

Because cryptocurrency is a financial instrument, it requires an analysis similar to that of stocks

. When cryptocurrency buyers make their choices, they analyze white papers or informational documents highlighting particular cryptocurrencies' aims and specialties. Hence, advertisement is crucial in influencing cryptocurrency buyers’ decisions aside from prices. However, because white papers are written by their developers, they are subject to scams, which I will also discuss later. In contrast, algorithms and models influence quantitative trading users’ decisions, making quantitative trading more precise and less deceitful. So, while humans teach holders how to use cryptocurrency, AI and programming languages teach users of quantitative trading platforms how to place their trade and how much thereof.

4.2. Risks and Regulation of Cryptocurrency

A combination of factors–funds diversion and volatility reports, hacking, leverage mismanagement, and market reactions

| [44] | Fu S, Wang Q, Yu J, et al. FTX collapse: a Ponzi story [C]//International Conference on Financial Cryptography and Data Security. Cham: Springer Nature Switzerland, 2023: 208-215. |

[44]

–led to the collapse of the Futures Exchange (FTX), one of the biggest cryptocurrency exchanges before bankruptcy. Below is a brief description of each

:

Volatility reports: Coindesk, a media company for cryptocurrency values and transactions, avowed that the native asset of FTX, FTX Token or FTT, experienced a decline in value.

Market reactions: Binance, the biggest cryptocurrency exchange, sold all FTT tokens. Customers started withdrawing their funds.

Leverage Mismanagement: FTX had borrowed too much money before, so they were undertaking extremely high debts after they misused and lost the money. FTX asked Binance for cash, but Binance did not lend it to protect the company from financial losses. When FTX anticipated an 8 billion dollar bailout, the authorities of the Bahamas suspended their activities.

Hacking: FTX surmised that about 477 million dollars were lost in the hot storage due to hacking.

Investigation reports: Authorities found that FTX transferred customer funds to its sister company, Alameda Research, without authorization. In addition, they discovered that FTX exaggerated the value of FTT tokens. As a result, customers’ trust was eroded, the liquidity crisis worsened, and the FTX collapse was marked as the effect of financial fraud.

Yet, the most fundamental cause of the FTX collapse was that the consensus value of FTT tokens declined. The prices of Bitcoin and Ethereum are consistently high because customers think they are usually worth a lot and will always buy and sell; consequently, they will seldom fall sharply.

Regulation is essential to prevent financial crises like the FTX collapse. That said, cryptocurrency is not entirely free of regulation. Exchanges must be approved with a license, and Anti-Money Laundering and Know-Your-Customer programs must be administered

. Still, many recent cryptocurrency tradings are facilitated by criminals underground

. Regular auditing and education may assuage transparency issues in some cryptocurrency trading. However, as the International Monetary Fund (IMF) suggests, federal authorities should, at some point, investigate fraudulent activities by cryptocurrency owners

. They should enact laws that function as layers to regulate cryptocurrency holders. Laws can be like this: federal agencies must approve cryptocurrency developers if a cryptocurrency exchange tries to divert funds; otherwise, federal agencies will freeze the entire account. Financial issues are usually viewed from the perspective of a utilitarian, so the law would work since almost no one would sacrifice the greater good for individual interests.

Regulators should consider applying the Basel Framework to cryptocurrency regulation. A cryptocurrency is often equivalent to multiples of cash, so a loss of a cryptocurrency coin may be comparable to a loss of thousands of dollars. Regulators should admonish buyers about the amount of cryptocurrency they should purchase at once. Also, cash borrowing and lending are inevitable because of the high conversion factor. Considering the Basel Framework, fiat money leverage should be limited for cryptocurrency buyers, and customer funds of cryptocurrency exchanges should be misappropriated within the scope of buffer capital. In developing markets, regulators like the SEC can consider offering crypto-assets themselves or asking central banks to provide cryptocurrency services, thereby giving more people access to cryptocurrencies while supervising them

| [40] | Drakopoulos, Dimitris, Fabio Natalucci, and Evan Papageorgiou. 2021. “Crypto Boom Poses New Challenges to Financial Stability.” |

[40]

.

FTX’s CEO, Sam Bankman-Fried, asserted that the leverage mismanagement and liquidity issues were due to “poor internal labeling;” in other words, they miscalculated the numbers. That being said, cryptocurrency trading can consider ushering in AI and programming languages that develop mathematical formulas to resolve this concern. Cryptocurrency exchanges should also consider introducing backtesting to cryptocurrency trading; in such a way, speculative trading is reduced, which underpins customers’ trust.

Meanwhile, there are technical risks in cryptocurrency as well. The computer system's reorganization may cause the nodes to be cut off suddenly, causing both cryptocurrency coins and fiat funds to disappear. Someone I know lost two Bitcoins due to this issue.

5. Conclusion

Quantitative and cryptocurrency trading are more efficient than traditional hands-on trading. Innovative information technologies have built fast and extensive trading platforms, where a massive amount of data and funds can be exchanged within one trade in a shorter duration.

Everything has two sides. Quantitative and cryptocurrency trading is prone to systemic failures and transparency issues. From a computer glitch, much data and funds can be lost instantly, as Knight Capital did in 2012, leading to market crashes, client withdrawals, and company bankruptcies. From financial fraud, liquidity crises arose, as FTX did in 2022.

Because cryptocurrency is decentralized and liability-driven, centralized conventional financial policies should be imposed to regulate cryptocurrency

. This means that federal agencies must be educated on blockchain technology and know what laws and fiscal and monetary policies are appropriate for regulation. When devising centralized policies, regulators can refer to those enacted by the Chinese supervisory organizations. According to John Stuart Mill’s Harm Principle, the government should intervene because intervention minimizes harm, that is, illegal underground trading practices that imperil national security. The Basel Committee has already set international standards: they promulgated Basel IV in 2023, making leverage and capital ratios more strict

.

In contrast, because quantitative trading is fast, frequent, precise, and data-driven, nontraditional financial policies are necessary to control it. This means that the Basel Committee should consider adding policies that will check the power of technologies. However, this engenders another issue: regulators would stifle efficiency when they limit the speed and the amount of data that can be processed. In addition, regulators should set a high entrance bar to ensure the employment of qualified quantitative traders.

The quantitative finance industry will complement other financial technologies in enhancing financial inclusion. Hedge-fund chief Mark Yusko stated that cryptocurrency will reduce the global economic disparity

. In developing countries, cryptocurrency provides loans for those who do not have bank accounts, which help them access resources like clean water. As a matter of fact, cryptocurrency has set a path for 1.7 billion people to get out of poverty. In all of the cryptocurrencies, Bitcoin and Ethereum stand out for buyers in developing countries. This again reinforces the role of a consensus value in determining the market price of a cryptocurrency. Hence, the value of Bitcoin and Ethereum will persist high, and the regulation for these cryptocurrencies will be stricter than others.

The author foresees a bright future of quantitative trading. Despite the risks and challenges, quantitative trading pushes the limit of almost every aspect of trading. Technological prowess has accomplished what humans alone cannot; precisely, the speed, the volume, and the precision. But, like any software system, quantitative trading platforms demand advances. Companies should acknowledge that old technologies can no longer suffice and necessitate the development of new technologies to replace them. “Practice is the sole criterion of testing truth

.” Therefore, experiments are essential to paving the roads for the development of quantitative trading.

To conclude, AI, Blockchain, and many other information technologies will support the momentum of the Fintech industry. Research has shown that in the next five years, the Fintech industry's revenues will grow three times faster than the traditional banking industry's revenues

. Fintech’s rapid expansion also demonstrates inclusivity towards various socio-economic groups. Traditional banks are transitioning as well: 73 percent of the world interacts with banks online

. Financial technologies will continue to solve human issues once they are used properly.